The Reserve Bank of India (RBI) on May 29, 2024 imposed restrictions on ECL Finance (ECL) and Edelweiss Asset Reconstruction (EARC) for extensive mismanagement, confirming the grave concerns felt by some sections of the financial sector regarding the Edelweiss group for at least a decade. The RBI directed ECL “to cease and desist with immediate effect from undertaking any structured transactions” regarding its wholesale exposures. The regulator also ordered EARC, with immediate effect, to cease all business pertaining to financial assets, including Security Receipts (SR).

Shareholders of Edelweiss Financial Services (EFS), the listed holding company of the group, and stakeholders of its unlisted subsidiary ECL, perusing the ECL annual report, were presented with a rosy picture of compliance, accountability, transparency and ethical behaviour. ECL’s FY2023 annual report states,

“We believe that compliance is not just a box to be ticked, or a set of regulations to be followed; it is an integral part of who we are as an organisation, deeply ingrained in our DNA shaping every single action of ours. Our commitment to compliance begins at the top, with a strong governance structure that emphasises transparency, accountability, and ethical behaviour At ECLF [ECL], Compliance is everybody’s business…We promote a culture of accountability, transparency and ethical conduct across the Company. The policy establishes overarching principles and commitment to action – to achieve compliance in letter and spirit…” (p. 28-29)

In contrast to this flattering self-portrait, the regulator has exposed the extremely serious issues in the Edelweiss group, and caustically observed that the company was,

“acting in concert by entering into a series of structured transactions for evergreening stressed exposures of ECL… [the NBFC was submitting] incorrect details of its book debts to its lenders for computation of its drawing power, non-compliance with loan to value norms for lending against shares, incorrect reporting to Central Repository for Information on Large Credits system (CRILC) and non-adherence to Know Your Customer (KYC) guidelines. ECL, by taking over loans from non-lender entities of the group for ultimate sale to the group ARC, allowed itself to be used as a conduit to circumvent regulations which permit ARCs to acquire financial assets only from banks and Financial Institutions.”

The sharp divergence between ECL’s professions of ethical behaviour and the regulator’s findings on the entire group renders any public commentary by the group irrelevant and completely misleading. The systemic mismanagement in the group should result in the sacking of the senior executive management and the restructuring of the respective boards of directors. When the regulator publicly exposes such alarming practices in a financial group, a change of ownership and management is essential to restore stakeholders’ confidence.

The RBI’s observations also cast a very poor light on the internal and external auditors of ECL and EARC. In FY2022 and FY2023, ECL’s external auditors were M/s Chetan T Shah and M/s V.C. Shah, while for EARC in FY2023 it was Nangia and Co. The first warning bells should have been rung by the auditors, and the audit committees of the boards should have immediately addressed these issues. But it appears from the RBI’s commentary the group had no intention of addressing these major concerns.

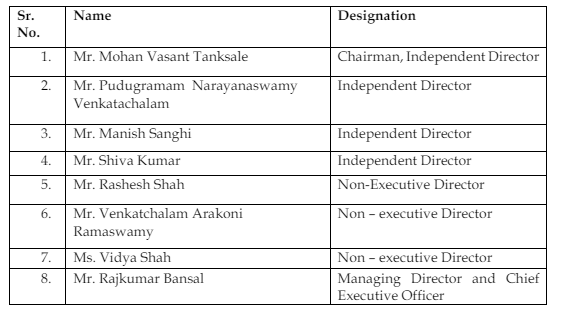

In terms of professional competence and experience, the ECL board of directors appeared sound on paper. The chair and vice-chair were founder non-executive directors, and the independent directors (IDs) amongst others were Shiva Kumar, a former career State Bank of India (SBI) commercial banker; B. Mahapatra, a former Executive Director of RBI, Aalok Gupta, a former foreign and private sector commercial banker, and K Chinniah, an individual with global private equity experience. These select IDs had prior commercial and investment banking experience and should have been well versed with regulation, risk and compliance management. All these IDs with the exception of Aalok Gupta were also members of the all-important audit committee of the board. Interestingly, Shiva Kumar, Mahapatra and Chinniah were also directors of Edelweiss Financial Services, the holding company, and therefore would have had a more comprehensive knowledge of the entire group.

ECL Finance Board of Directors

| FY2022 | FY2023 | |

| Non-Exec. Chairman | Rashesh Shah (co-founder) | |

| Non-Exec. Vice-Chairman | Venkatchalam Ramaswamy (co-founder) | |

| Exec. Vice Chairman | Deepak Mittal | |

| Managing Director | Phanindranath Kakarla | |

| ED | – | Mehernosh Tata |

| Nominee Director | Anita George | |

| Independent | P N Venkatachalam (ex SBI) | – |

| Independent | – | Shiva Kumar (x SBI) |

| Independent | – | Sameer Kaji |

| Independent | Biswamohan Mahapatra (x ED, RBI) | |

| Independent | – | Atul Pande |

| Independent | – | Aalok Gupta (banking) |

| Independent | Kunnasagaran Chinniah (x GIC, Singapore) | |

Source: ECL Finance

ECL Finance Audit Committee

| FY2022 | FY2023 | |

| Chairman | Biswamohan Mahapatra (x ED, RBI) | |

| Nominee Director | Anita George | |

| Independent | Kunnasagaran Chinniah (x GIC, Singapore) | |

| Independent | – | Shiva Kumar (x SBI) |

| Independent | – | Sameer Kaji |

| Independent | P N Venkatachalam (ex SBI) | P N Venkatachalam (ex SBI) till 16.9.22 |

Source: ECL Finance

Edelweiss Financial Services Board of Directors

| FY2022 | FY2023 | |

| Chairman & CEO | Rashesh Shah (co-founder) | |

| Vice-Chairman & ED | Venkatchalam Ramaswamy (co-founder) | |

| ED | Himachu Kaji | |

| ED | Rujan Panjwani | – |

| Non-Exec, Non-indep. | Vidya Shah (finance, wife of Rashesh Shah) | |

| Independent | P N Venkatachalam (ex SBI) | – |

| Independent | Navtej Nandra (investment banking) | – |

| Independent | Kunnasagaran Chinniah (x GIC, Singapore) | – |

| Independent | Biswamohan Mahapatra (x ED, RBI) | |

| Independent | Ashok Kini (x SBI) | |

| Independent | Ashima Goyal (economist) | |

| Independent | Shiva Kumar (x SBI) | |

Source: Edelweiss, Social media

Edelweiss Financial Services Audit Committee

| FY2022 | FY2023 | |

| Chairman | P N Venkatachalam (ex SBI) | Shiva Kumar |

| Independent | Biswamohan Mahapatra (x ED, RBI) | |

| Independent | Kunnasagaran Chinniah (x GIC, Singapore) | – |

| Independent | Ashok Kini (x SBI) | |

| Independent | Berjis Desai (till 6.11.2021) | Ashima Goyal (economist) |

Source: Edelweiss

Edelweiss ARC Board of Directors in FY2023

Source: Edelweiss ARC

Audit Committee of Edelweiss ARC as on March 23, 2023

Source: Edelweiss ARC

The question is, what were these IDs, with their wealth of professional experience, doing when the companies were brazenly violating all regulatory norms? No doubt, in one particular instance the regulator has recorded that the RBI’s inspection report pertaining to FY2022 was not placed before the EARC board by the management, which is a mandatory requirement. In this particular case the board can be absolved; but in all the other cases the IDs needed to constantly ask probing questions and demand data from the executive. The board of directors of Edelweiss Financial Services, the holding company of the group, and the boards of ECL and ECLF have to be held accountable. The companies had experienced individuals as IDs, and they cannot plead ignorance or even say that the executive did not inform the board, as oversight is their fiduciary duty.

When the regulator publicly documents widespread mismanagement in a regulated entity, it signifies that IDs are either incompetent or are complicit with the management. In either case they are unfit to be directors in any company.

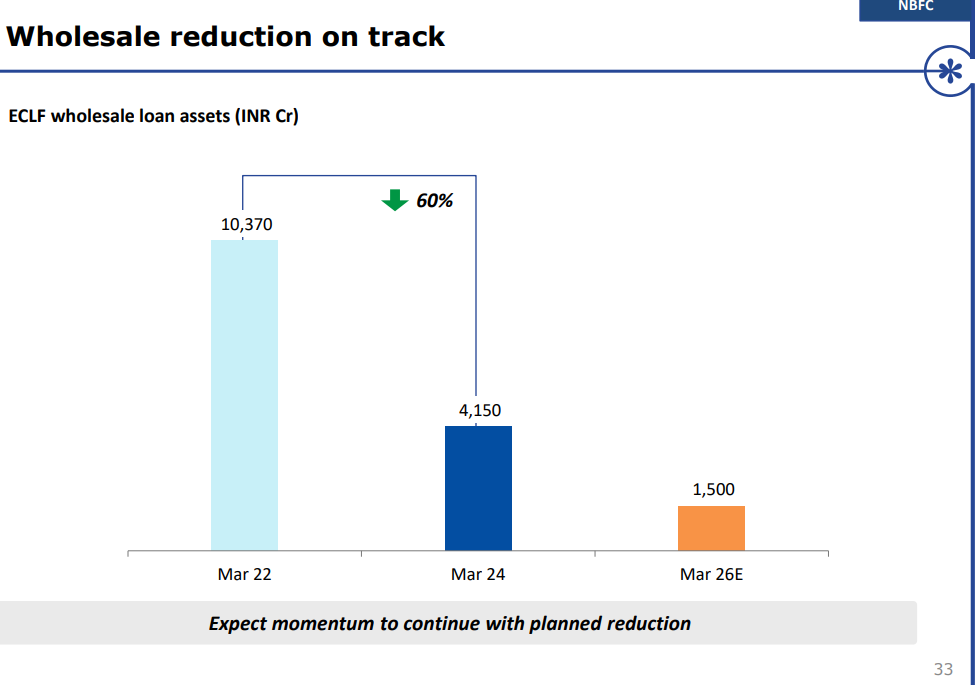

The business strictures imposed by the RBI may not be onerous for ECL, as the NBFC has been winding down its wholesale business in the last few years on account of asset quality and possible regulatory issues. In FY2024, the wholesale book declined by 60% from the previous year to Rs 41.5 bn, and it was projected (even prior to the RBI censure) to reduce to Rs 15 bn in FY2026.

Source: Edelweiss Finance

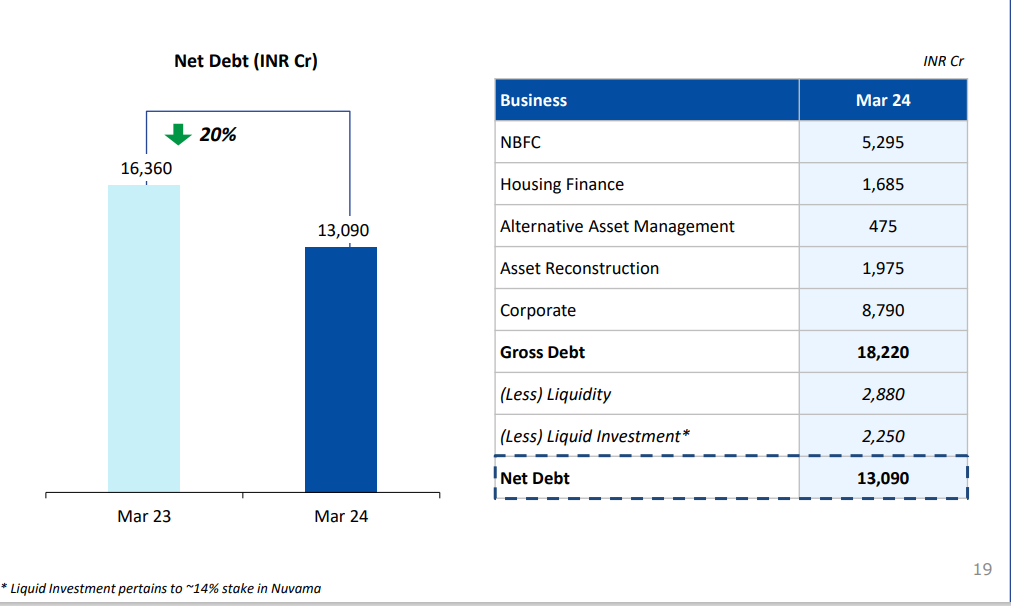

In the wake of RBI’s penalising ECL and EARC, and more importantly, publicly documenting major instances of violations, the reputation of the entire group is discredited. Reputational risk leading to liquidity risk is going to be a major issue for the Edelweiss group. When the regulator states that the group was “evergreening stressed assets of ECL”, using group platforms to circumvent regulations, submitting incorrect details of its eligible book debts to lenders for calculation of drawing power, and other violations, it raises serious concerns for the group’s lenders. The bulk of NBFC borrowings is normally from commercial banks, followed by the debt market.

Source: Edelweiss Finance

As per the 4QFY2024 results disclosure (prior to the RBI action), the group has reported a comfortable asset-liability position in all the three buckets; less than 1 year, 1-3 years and 3 years plus. In FY2025 it requires fresh borrowings of Rs 24 bn, and expects inflows of Rs 88 bn. However, as the regulator has stated that ECL misrepresents its accounts, these numbers too cannot be relied upon by the group’s lenders. Following the RBI action, bank lenders to the group may demand a forensic audit of the group. They can be expected to immediately curtail existing credit lines and reduce their exposure, increasing the liquidity risk for the group. The option of raising of debt through commercial paper, particularly from debt mutual funds, will be immediately shut, as managers of public funds will not provide any additional funds to an entity which has been severely penalised by the regulator, even more so when, as in this case, the veracity of the company’s financial accounts is in doubt. For raising additional debt, the group may have to approach special situation funds, which charge usurious rates, sharply raising the cost of funds for the group.

Edelweiss Group Liquidity

Source: Edelweiss Finance

An unusual regulatory development in RBI’s interaction with EARC is that, in an inaugural address to chairpersons, directors and Chief Executive Officers of ARCs on May 17, 2024, Swaminathan J, deputy governor, RBI highlighted that the culture of integrity and ethics flows from the top of an organisation, and hence “chairpersons, board of directors and CEOs can lead by example.” However, while the RBI acknowledges that the management of EARC did not present its (RBI’s) FY2022 inspection report to the board of directors, and that the company continued to circumvent regulations instead of complying with them, the RBI was engaged only with the senior management and the company’s auditors. If the RBI believes that integrity and ethics flow from the board of directors, then, given the fact that the EARC management had deliberately withheld RBI’s inspection report from the board of directors and given EARC’s extensive mismanagement, the regulator should have directly engaged with the chairman of the board and the independent directors, instead of restricting itself to only the untrustworthy senior management and the firm’s equally unreliable auditor.

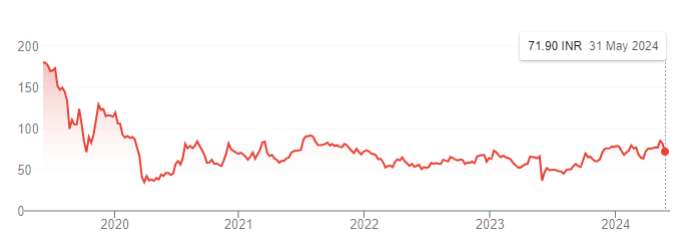

5-Year Share Price History of Edelweiss Financial Services

Source: Google Finance

In any market, the regulator must be both respected and feared, and it is commendable that the RBI is cracking the whip on regulated entities who are repeat offenders and show disdain for regulation, such as Paytm Payments Bank, Kotak Mahindra Bank, JM Financial, IIFL Finance and the Edelweiss group. For many years, there were concerns regarding the market practices of some of these entities, but ‘feather touch’ regulation and supervision allowed them to continue without severe regulatory censure. One hopes that the RBI’s recent actions, and their impact on the share prices of errant firms, discipline these institutions and demonstrate the regulatory fist to all participants in this strategically important sector.

This article was also published in The Wire and can be read here

_________________________________________

DISCLOSURE

I, Hemindra Kishen Hazari, am a Securities and Exchange Board of India (SEBI) registered independent research analyst (Regd. No. INH000000594). Please see SEBI disclosure here. Investment in securities market are subject to market risks. Read all the related documents before investing. Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. The securities quoted are for illustration only and are not recommendary. I own equity shares in Kotak Mahindra Bank. Views expressed in this Insight accurately reflect my personal opinion about the referenced securities and issuers and/or other subject matter as appropriate. This Insight does not contain and is not based on any non-public, material information. To the best of my knowledge, the views expressed in this Insight comply with Indian law as well as applicable law in the country from which it is posted. I have not been commissioned to write this Insight or hold any specific opinion on the securities referenced therein. This Insight is for informational purposes only and is not intended to provide financial, investment or other professional advice. It should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security.

All rights reserved. No portion of this article may be reproduced in any form without permission from the author. For permissions contact: