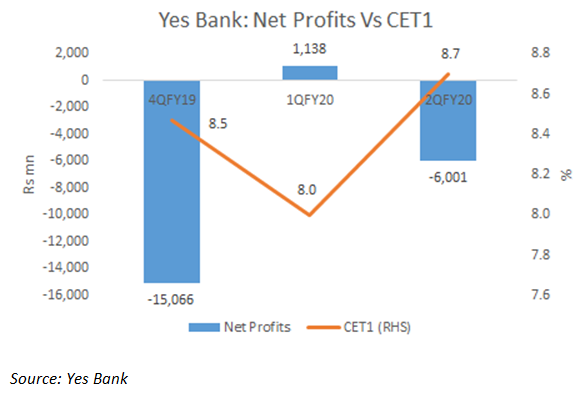

EXECUTIVE SUMMARY. In a significant set-back, Yes Bank reported that its accounts for FY2019 were fudged: the banking regulator had detected under-reporting of non-performing loans and credit costs and over-stating of profits by the bank. This development is disturbing, as it undermines the credibility of Ravneet Gill, the new CEO (took charge on March 1, 2019), the audit committee (chaired by independent director, Uttam Prakash Agarwal), Venkataramanan Vishwanath, partner, B S R & Co. (member firm of KPMG) and the office of the Chief Financial Officer (the then CFO, Raj Ahuja was replaced in August 2019). The timing of this development is particularly unfortunate, as the bank desperately seeks additional equity capital and has to date not finalised the issue. This news will cast a negative light on the credibility of its accounts.

The only charitable explanation is that, since Gill took charge on March 1, and the accounts were finalised on April 26, he may have had inadequate time and exposure to closely monitor some of the corporate accounts which the bank had imprudently classified as performing. Nevertheless, given the bank’s legacy of dodgy accounts (in FY2016 and FY2017) and various publicly documented corporate governance lapses by Rana Kapoor, the erstwhile founder-CEO, Gill should have exercised extra caution and been more prudent in maintaining the integrity of the bank’s accounts. It is shameful for any bank and its CEO to be publicly hauled up by the banking regulator for fraudulent accounts, and wilful mis-reporting by a bank is a criminal offence as per the law of the land. Stakeholders can only hope that, as Gill settles down, he will restore the sanctity of the bank’s accounts and that FY2019 was the departing legacy of the past.

Under Mr Kapoor, total assets of the bank grew at a compound annual growth rate of 34 per cent in the 10 years through March 2018, outpacing peers. But a crackdown by the central bank on a system-wide legacy of shoddy lending led to action against several lenders. Yes Bank has argued that the impact of its so-called bad-loan divergence was small because many loans classified as problematic by the RBI were subsequently recovered.